Resources

Guide to Setup Bangladesh Business

Human Resource Immigration

Industry Guide

Entrepreneurship

Miscellaneous Topics

Bangladesh Industry Digital Plan

Corporate Compliance Requirement

Finances and Grants

Bangladesh Taxation

Balance Management Control With Limited Liability Partnership

In a limited liability partnership, the partners are limited in their liability. The partnership combines the features of a partnership and a corporation. According to law, an LLP does not make its partners responsible or liable for their misconduct or negligence.

The liability of partners in an LLP can sometimes be limited, similar to that of shareholders in a corporation. A general partner may need to have unlimited liability in some states, which means that he/she is responsible for the business’s debts as well as lawsuits such as personal injury or breach of contract. Business management is handled directly by the partners, not by corporate shareholders. Corporate shareholders elect their board through various state charters. The board organizes itself and hires corporate officers, who are legally obligated to govern the corporation in the corporation’s best interest. The tax liability of an LLP differs from the tax liability of a corporation.

Smoothly Establish a Limited Liability Partnership with Network BD

Our limited liability partnership (LLP) services are tailored to the individual needs of each client. Due to the fact that LLPs are a new regulation in India, we support clients from the very beginning of the LLP formation process to its ongoing maintenance, and so on.

Among the services we provide are:

- Managing the formation of a limited liability partnership

- Providing alerts, circulars, and updates on LLP laws.

- Managing the timely electronic filing of relevant paperwork with the registrar.

- Maintaining statutory records and filing them with the registrar in a timely manner.

- Assisting with charge registration, adjustment, and payment.

- Assisting in the acquisition of designated partner identification numbers (dpins) and digital signatures for the filling of llp online forms.

Core Features Of LLPs Process

A limited liability partnership is a hybrid of a corporation and a partnership. It possesses the characteristics of both of these types. As the term implies, partners have limited liability in the firm, which means that their personal assets are not used to pay off the company’s debts. It has become a very popular form of company in recent years, with many entrepreneurs opting for it. Because there are several partners in the firm, they are not liable or responsible for the actions of others. Each person is responsible for their own actions.

It, like companies, has its own legal entity.

Each partner’s responsibility is restricted to the amount of his or her contribution.

Creating an LLP is inexpensive.

There are fewer rules and regulations to follow.

There is no minimum capital contribution requirement.

An LLP must have at least two partners to be formed. The maximum number of partners in an LLP is unrestricted. A minimum of two designated partners who are people should be among the partners, with at least one of them residing in Bangladesh.

The LLP agreement governs the rights and responsibilities of chosen partners. They are personally responsible for ensuring that the terms of the LLP Act 2008 and the LLP agreement are followed.

If you wish to form a firm as a Limited Liability Partnership, you must register it under the Limited Liability Partnership Act.

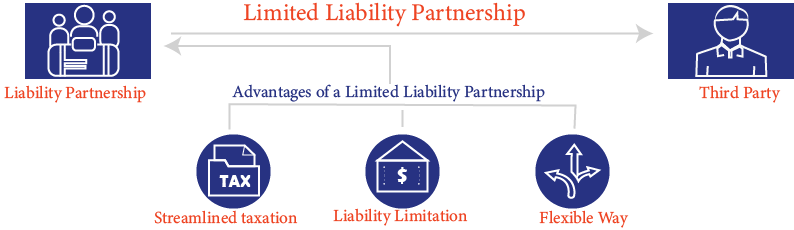

Special 3 Advantages of a Limited Liability Partnership

1. Streamlined taxation:

It is business partners who claim the company’s deductions and credits on their personal tax returns. Credits and deductions are based on the percentage of individual interest each partner has in the company.

2. Liability Limitation:

LLPs shield limited partners from personal liability resulting from negligent acts committed by other limited partners or employees who are not under their direct control. The result is that partners do not personally bear the costs of debt or other obligations of the company.

3. Flexible:

Limited liability partnerships allow partners to own the company to the extent they want. Regardless of how each individual contribution to business operations are funded and enacted, partners have the ability to make their own decisions. It depends on the experience of the partners whether management responsibilities should be split equally or unequally. Company partners who own a financial interest in the company can choose not to have any authority over business decisions but still retain ownership rights based on their percentage stake.

Documents Required For LLPs

LLP’s paperwork

1. During registration or within 30 days of incorporation, proof of registered office must be given.

2. A rent agreement, as well as a no-objection certificate from the landlord, must be filed if the registered office is taken on rent. The landlord’s consent to the LLP using the space as a registered office’ will be represented by a no-objection certificate.

3. Furthermore, any utility bill, such as gas, electric, or telephone bill, must be submitted. The bill must include the full address of the property as well as the name of the owner, and it must be less than two months old.

4. Because all documents and applications will be digitally signed by the authorized signatory, one of the chosen partners must also choose a digital signature certificate.

How Limited Liability Work For You?

LLPs protect non-negligent public accountants’ personal assets, such as homes and RRSPs, under the Partnership Act. In an LLP, each partner is responsible for their own mistakes. However, if another partner causes carelessness, wrongful acts or omissions, malpractice, or misconduct, a non-negligent partner’s personal assets are not subject to the partnership’s debts and liabilities. All other debts and liabilities of the partnership are the responsibility of all partners.